Budgeting your bi-weekly paycheck is a fundamental skill for financial stability and success. Whether you’re saving for a big purchase, paying off debt, or simply trying to manage your expenses efficiently, creating and sticking to a budget is essential. In this guide, we’ll walk you through the steps to effectively budget your bi-weekly income.

Understanding Your Income:

Before you can start budgeting, it’s important to understand exactly how much money you’re bringing in with each paycheck. Your gross income is the total amount you earn before taxes and other deductions. Your net income, on the other hand, is what you actually take home after taxes and deductions are withheld. Knowing your net income is crucial for creating a realistic budget.

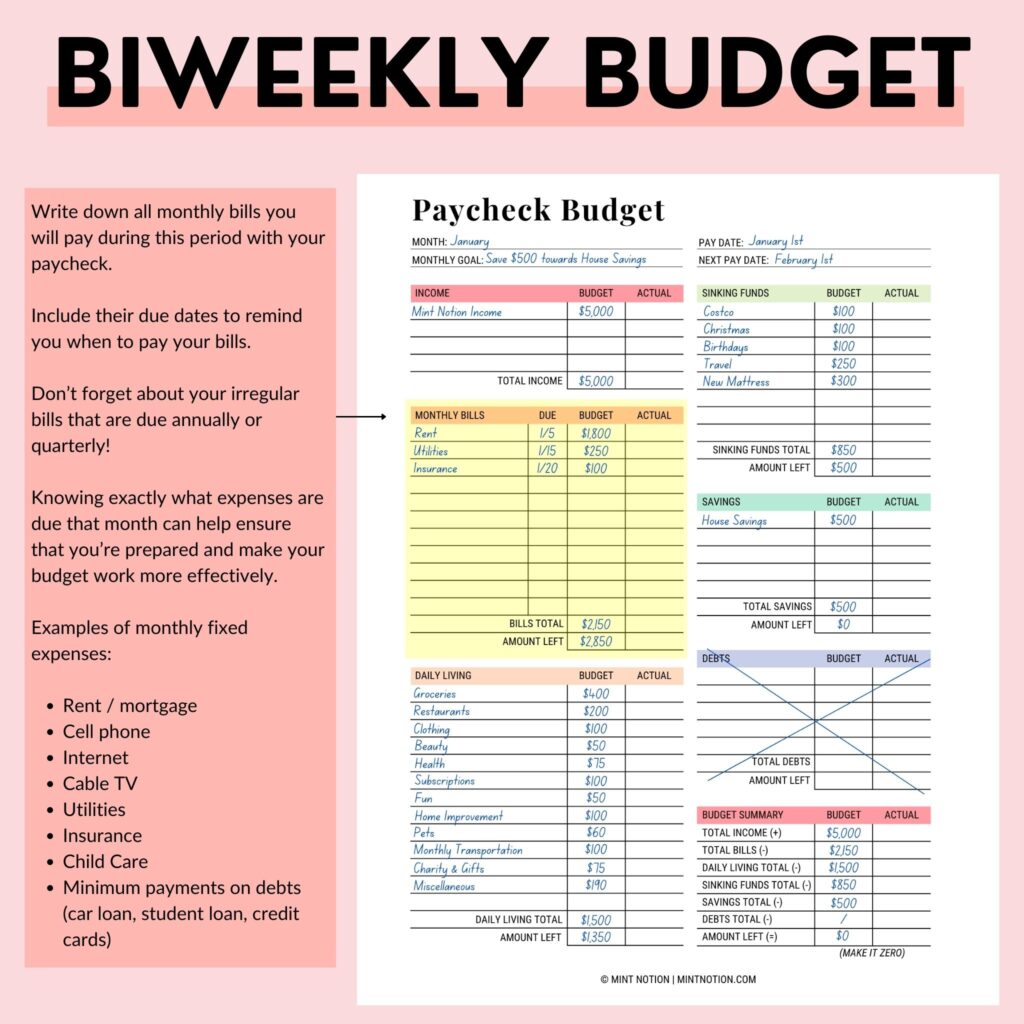

Step 1: Determine Fixed Expenses

Start by identifying your fixed expenses, which are regular payments that stay relatively constant from month to month. These may include rent or mortgage payments, car payments, insurance premiums, utilities, and subscription services. Add up the total amount of your fixed expenses for the month.

Step 2: Account for Variable Expenses

Variable expenses are costs that fluctuate from month to month. These might include groceries, dining out, entertainment, transportation, and other discretionary spending. To budget for variable expenses, review your spending habits from previous months and estimate how much you typically spend in each category.

Step 3: Set Aside Savings

Saving money should be a priority in any budget. Aim to allocate a portion of each paycheck to savings, whether it’s for an emergency fund, retirement, or a specific financial goal. A common recommendation is to save at least 20% of your income, but adjust this percentage based on your individual financial goals and circumstances.

Step 4: Plan for Debt Repayment

If you have debt, such as student loans, credit card debt, or a car loan, allocate a portion of your budget to debt repayment. Make minimum payments on all debts to avoid penalties, and if possible, allocate extra funds to pay down high-interest debt more quickly.

Step 5: Allocate Remaining Funds

After accounting for fixed expenses, variable expenses, savings, and debt repayment, allocate the remaining funds in your budget to discretionary spending. This could include non-essential purchases like dining out, shopping, or entertainment. Be mindful of your spending in this category and adjust as needed to stay within your budget.

Step 6: Monitor and Adjust

Budgeting is an ongoing process, not a one-time task. Monitor your spending regularly to ensure you’re staying on track with your budget. If you find that you’re consistently overspending in certain areas, adjust your budget accordingly. Likewise, if you have extra funds available, consider reallocating them to savings or debt repayment to accelerate your financial goals.

Conclusion:

Budgeting your bi-weekly paycheck is a key step towards achieving financial stability and reaching your long-term financial goals. By understanding your income, identifying expenses, prioritizing savings, and monitoring your spending, you can take control of your finances and build a solid foundation for the future. With discipline and diligence, you can master the art of budgeting and enjoy greater financial freedom.